The cheapest path is usually Public Service Loan Forgiveness, assuming your employer qualifies and you can stay ten years. Outside of that, paying the loans off aggressively beats every income-driven option once you account for the tax bill on the forgiven balance.

When I graduated with $180,000 in loans, nobody handed me a clear breakdown of what each option actually costs. This is what I wish I'd had.

The Scenario We're Using

To make sure we are comparing apples to apples, every number below uses the same scenario:

- Student loan balance: $150,000

- Interest rate: 6.5%

- Income: $90,000 AGI (averaging a starting salary around $75k that grows to $110k over 20 years)

- No dependents

Your numbers will be different. Use the calculator to model your specific situation, but this gives us an apples-to-apples comparison across all three paths.

| Strategy | Years | Total Cost | Notes |

|---|---|---|---|

| PSLF | 10 | $90,000 | Tax-free forgiveness if you qualify. |

| Pay It Off (refinanced to 5%) | 7.5 | $180,227 | Assumed $2,000/month payment. No forgiveness, no tax bill. Can be shortened with higher monthly payments. |

| New IBR | 20 | ~$196,600 | Includes an estimated $63,600 tax bill on forgiveness. Unpaid interest accrues and grows the forgiven balance. |

| RAP | 30 | $315,000 | Includes an estimated $45,000 tax bill on forgiveness. RAP costs $135,000 more than just paying it off. |

Scenario: $150,000 balance · 6.5% rate · $90,000 average AGI · no dependents

A Quick Note for Those Currently in PT, OT, or SLP School

Starting school after July 1, 2026? The rules changed. PT, OT, and SLP are classified as graduate programs instead of professional under the new "big beautiful bill." Federal loans are now capped at $20,500/year with a $100,000 lifetime limit. Grad PLUS loans are gone. Average PT school costs $108,000–$126,000 before living expenses. Most new students will need private loans to cover the gap.

Short version: pay private loans off first, don't refinance federal loans if you are considering PSLF, and then choose a federal strategy from the options below.

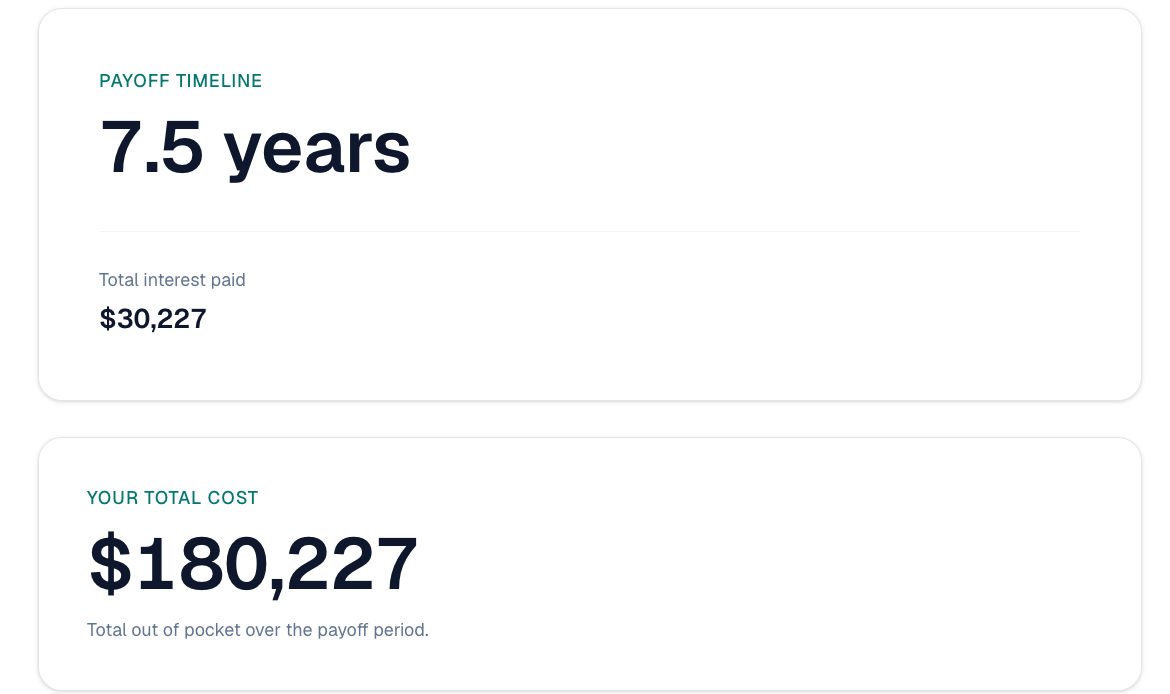

Option 1: Pay It Off

Trade: 7 to 8 years of aggressive payments for total flexibility after.

This is for the person who wants options above all else. Maybe you're planning to go part-time, have kids, open a private practice, or just want the freedom to walk away from any job at any time. You don't want your employer choices locked in for a decade, and you don't want a tax bill waiting for you in 20 years.

Total cost in this scenario: $180,227

(Refinanced from 6.5% to 5%, paying $2,000/month.)

- Pros: Total flexibility. No employer requirements, no multi-decade commitments. Refinancing lowers your rate and reduces total interest paid. If you decide to be more aggressive, you can dramatically cut this time down to just a few years.

- Cons: More expensive than PSLF if you'd qualify. Refinancing federal loans permanently removes them from any forgiveness program, so be certain before you do it.

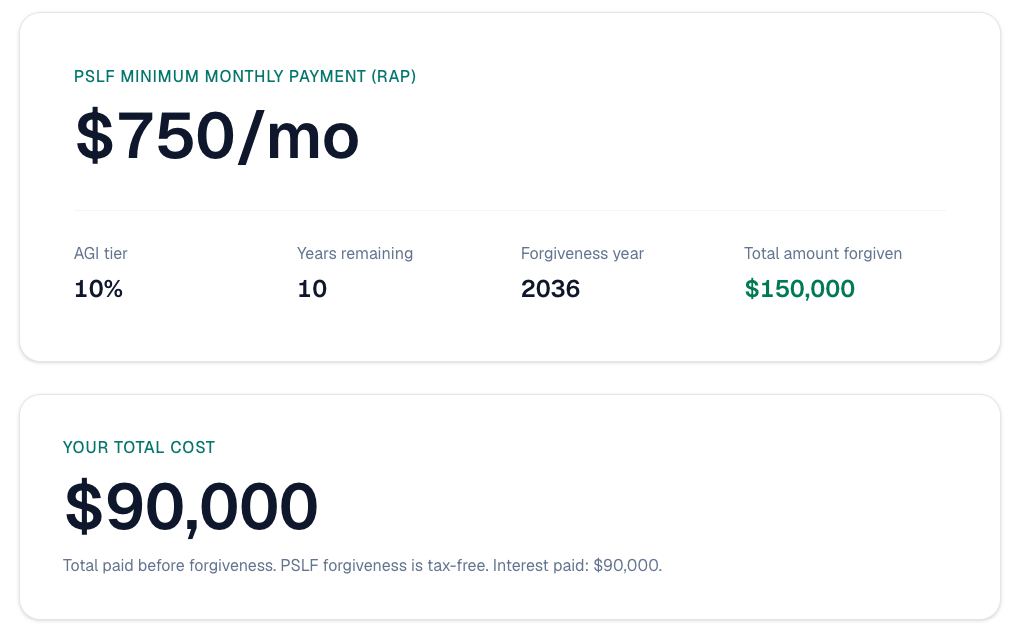

Option 2: Public Service Loan Forgiveness (PSLF)

Trade: 10 years at a qualifying employer for the lowest total cost.

This is for the person willing to commit to a public service setting, such as a hospital system, a school district, a nonprofit clinic. You're not planning to bounce around. You want the absolute lowest total cost of repayment, and you can live with the structure of a 10-year commitment.

Total cost in this scenario: $90,000

(10 years of income-driven payments. $150,000 forgiven tax-free at the end.)

- Pros: Lowest total cost by a wide margin if you qualify. Tax-free forgiveness. Payment is based on income, not your balance. You can reduce your AGI and therefore your monthly payment by contributing to your 401k.

- Cons: Full-time qualifying employment for 10 years. Payment increases as income grows. Smaller towns may have fewer qualifying employers. There are tax-filing implications if your spouse works.

- Critical: Do not refinance federal loans if you're pursuing PSLF. It permanently disqualifies those loans, no exceptions.

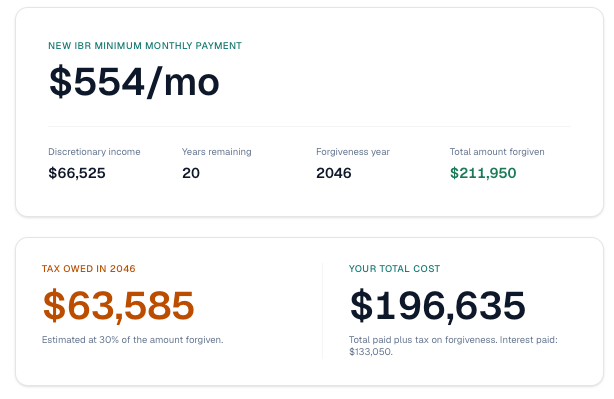

Option 3: Income-Based Repayment (IBR)

Trade: 20 years of manageable payments for a higher total cost and a tax bill at the end.

This is for the person in the private sector carrying significant debt relative to their income. You don't qualify for PSLF and you want a payment that stays manageable while your income builds. IBR keeps your monthly payment low, but there's a catch: when your payment doesn't cover the monthly interest, the unpaid interest piles up over the 20-year term. By the end of this scenario, your forgiven balance has grown from $150,000 to about $212,000, and the forgiven amount is taxable in the year it's discharged.

At very high debt loads relative to income, IBR can still beat paying it off even with the bigger tax bill. In this specific scenario, with $150k debt and a $90k average AGI, paying it off comes out about $16,000 cheaper. Run your own numbers. The threshold where IBR wins shifts with both the debt-to-income ratio and the interest rate.

Total cost in this scenario: $196,600

(20 years of payments at 10% of discretionary income. About $212,000 forgiven, with an estimated $63,600 tax bill.)

- Pros: Keeps payments manageable when income is lower. Works well when your debt is very high relative to income.

- Cons: Unpaid interest accrues over the 20-year term, so the forgiven balance and the tax bill grow over time. Annual recertification required. More expensive than PSLF by about $107,000 in this scenario.

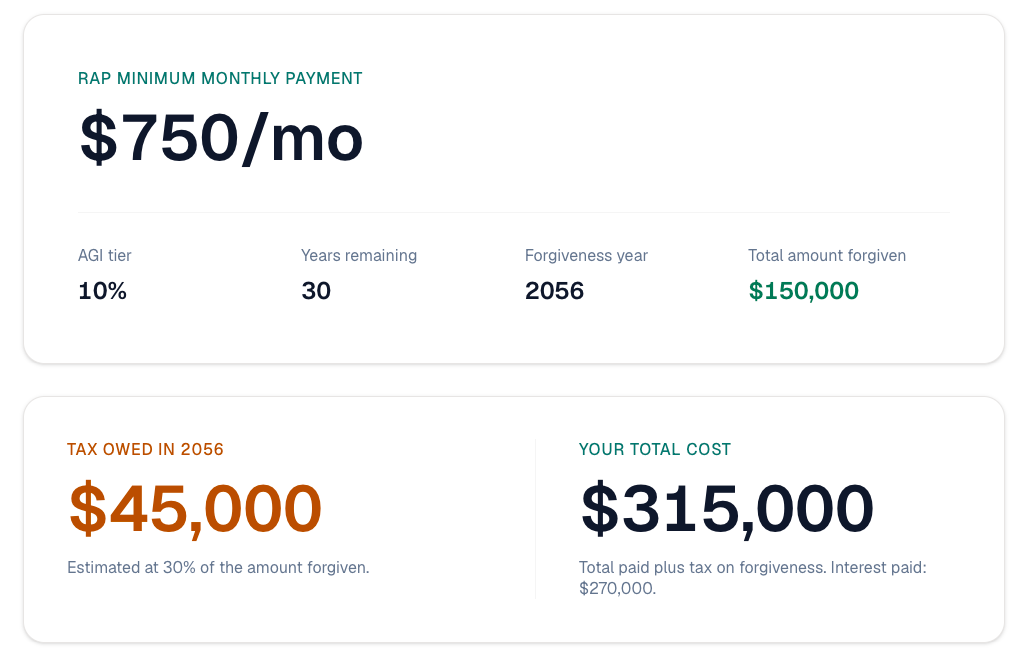

Repayment Assistance Plan (RAP) — 30-Year Forgiveness (Post-2026 Loans)

Trade: 30 years of low monthly payments for the worst total math of any option.

RAP without PSLF is not really a viable option after 2026. It is now the only income-driven option for new federal loans disbursed after July 1, 2026, thanks to the One Big Beautiful Bill (OBBB). If your loans were taken out after this date and you end up in the private sector, this is what you have. The math makes a strong argument for paying it off aggressively instead.

Total cost in this scenario: $315,000

(30 years of payments at 10% of AGI. $150,000 forgiven and an estimated $45,000 tax bill. Total cost is $135,000 more than just paying it off.)

- If you have post-2026 loans and end up in private practice: the case for paying it off fast is strong. RAP will cost you more in the long run, often significantly.

- If PSLF is an option: RAP counts as a qualifying repayment plan. Use it for PSLF, not for the 30-year forgiveness.

Which Path Is Yours?

- Working full-time at a hospital, nonprofit, or government agency long-term → PSLF. Ten years tied to a qualifying employer for the lowest total cost.

- Private sector, pre-2026 loans, very high debt relative to income → IBR. Twenty years of low payments and a tax bill at the end. Beats aggressive payoff only at high enough debt-to-income; run the numbers.

- Private sector, post-2026 loans → Pay It Off. Seven to eight years of aggressive payments. RAP is the only IDR alternative and costs $135,000 more in this scenario.

- Flexibility is non-negotiable, going part-time, having kids, switching settings → Pay It Off. Seven to eight years of intensity for total flexibility after, no employer or program strings attached.

- Not sure yet → IBR. Keeps options open while your career stabilizes. You can pay more than the minimum or pivot to aggressive payoff later.

Run your own numbers here:

Disclaimer

I'm a PT, not a financial advisor. This is not financial advice. Student loan decisions are personal and complicated. Please consult a qualified professional before making major moves.